CHECKOUT EXPERIENCES THAT MAXIMIZE & MULTIPLY SALES

Power Your Growth with Smarter Payment Processing

Accepting Credit Cards for Your Business with Confidence Means...

Choosing the industry-trusted secure merchant account designed for business owners.

Turning more “yes” decisions into completed transactions with optimized checkout

Leveraging advanced automation tools for passive cashflow 24/7/365

Receiving support from a dedicated Relationship Manager who is familiar with your account

Ready to Uplevel the Way

You Get Paid?

Start by booking a Free Consultation with DIRECTPAY Relationship Manager Jason Henke. Enter your information below to choose a time:

NOT ALL PAYMENT PROCESSORS ARE BUILT THE SAME...

The Way You Handle Checkout

Directly Impacts Your Revenue

Even small improvements can lead to meaningful gains in your bottom line.

We're here to help - with one-to-one support tailored to your business.

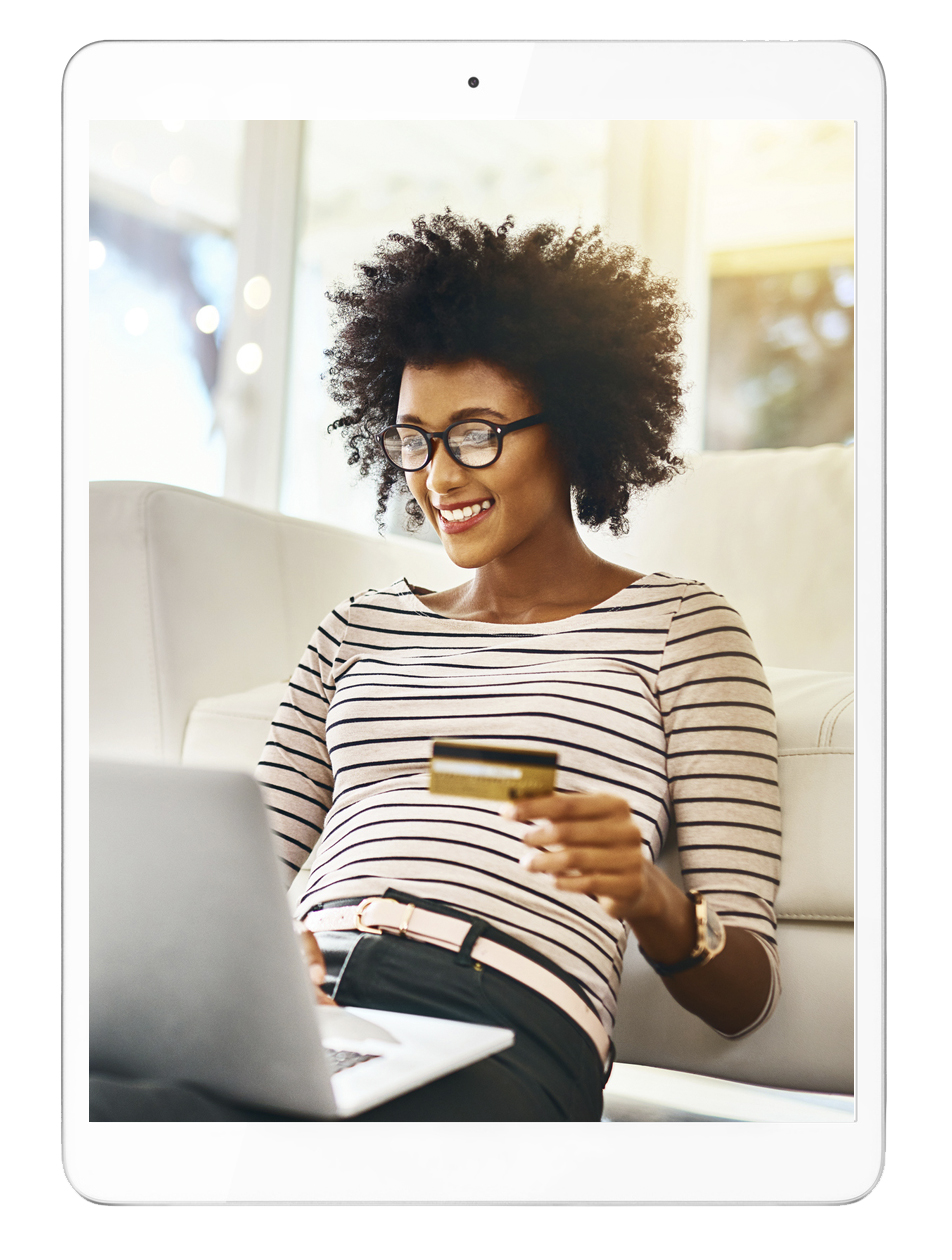

Credit Card Acceptance

For Worry-Free Transactions

Quick, secure payment processing with customized rates and advanced automation features powered by Authorize.Net.

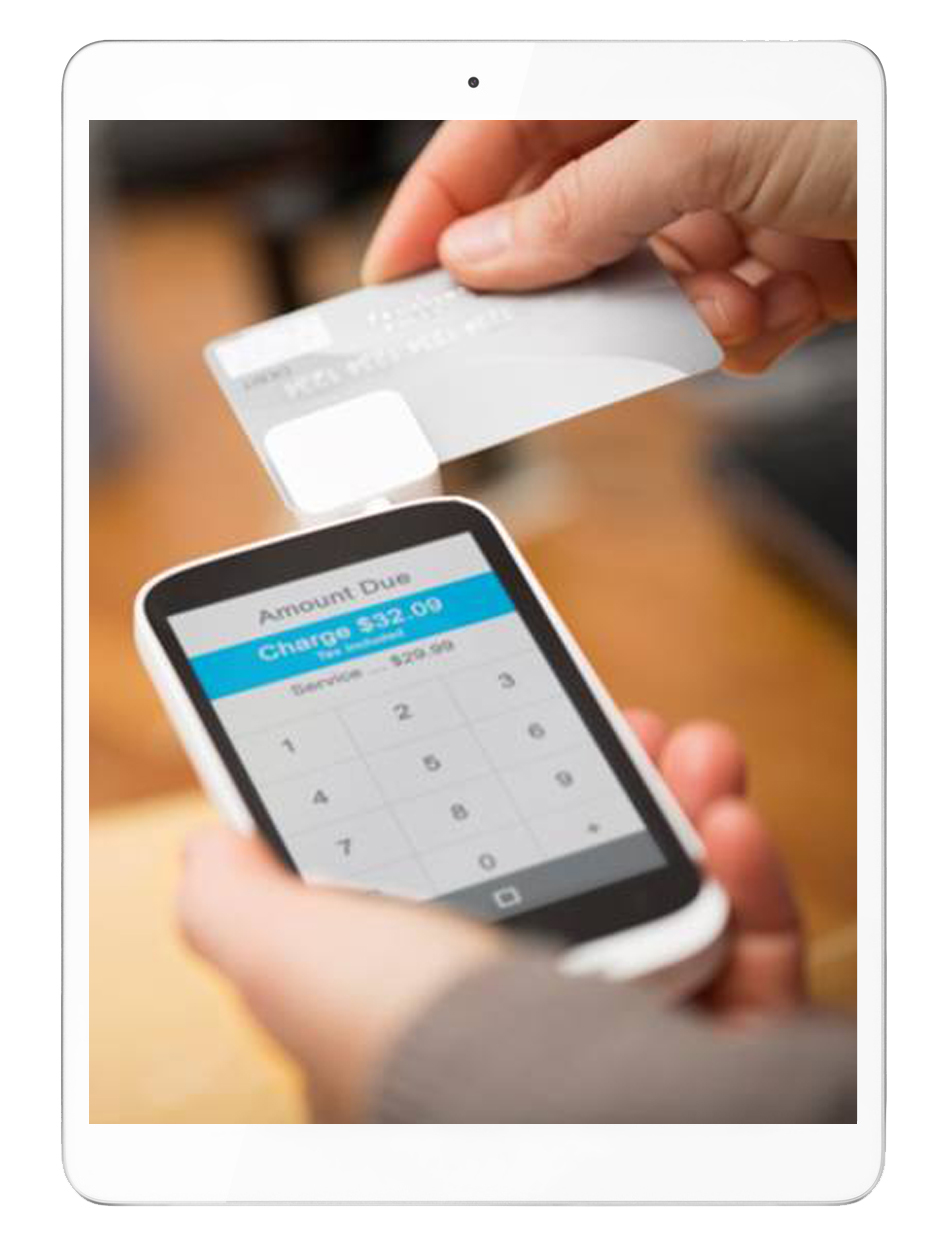

Mobile Payments

The Simple, Secure Swipe

Easy-to-attach reader and secure app to accept credit cards through your smartphone - wherever you do business.

APEX (HighLevel)

All-in-One Website & CRM

Powerful platform to manage contacts, funnels, sales, courses and more - everything you need to build, operate and grow.

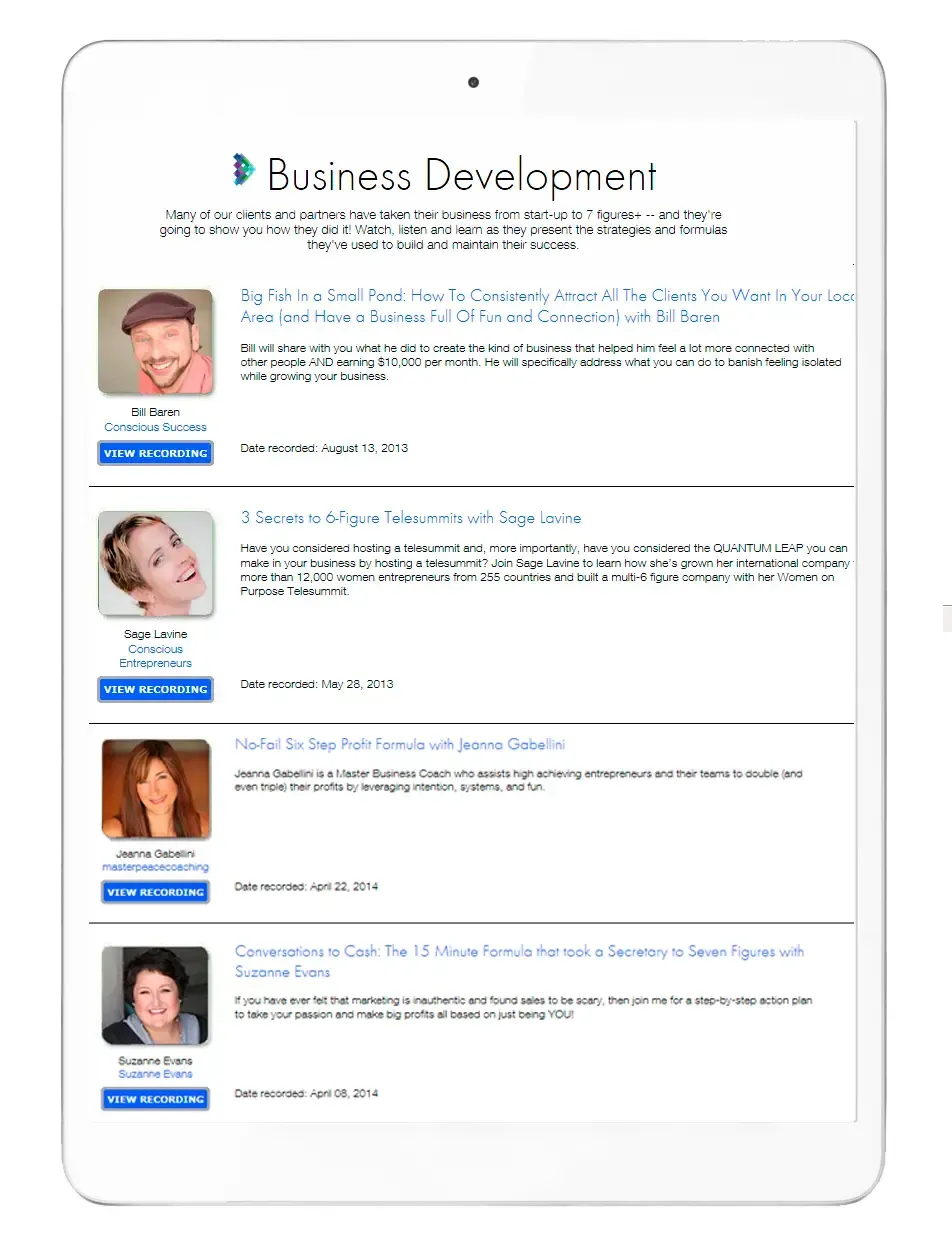

Business Development

7 Figure+ Success Secrets

Advice and inspiration from industry-leading entrepreneurs with action ready tips, ready-to-go templates and more!

WHAT'S DIFFERENT WITH DIRECTPAY?

More Than a Payment Processor:

A Revenue Partner

From hands-on support to growth-focused resources and meaningful connections, everything we do is designed to help your business run smoother and earn more.

One-to-One Support

Your Relationship Manager

You’re not routed through a help desk or left waiting on tickets.You have a dedicated Relationship Manager you know by name — someone familiar with your account, your business model, and how you get paid.

They actively monitor your account to help prevent disruptions like holds, delays, or chargebacks — so your revenue continues to move smoothly.

Guidance That Helps You Grow

Free Education & Strategy

We go beyond processing to help you improve how you sell and get paid. From training and strategy sessions to guest webinars with industry leaders, you’ll have access to insights that strengthen your business.

We also provide access to exclusive workshops and events — so you’re always learning, improving, and staying ahead.

Connections That Open Doors

Community & Partnerships

DIRECTPAY connects you with a community of business owners, partners and industry leaders.

Whether you're launching, scaling or collaborating, we help create opportunities through meaningful introductions and partnerships - because the right connections can lead to your next client, your next opportunity or your next level or growth.

Trusted by Industry Leaders

Our Featured Clients

"Signing up to accept payments with DIRECTPAY was one of the first things I did when I started my business and it was a smart decision.The service has been amazing; they've been with me every step of the way as I've grown from noting to now having a multi-million dollar coaching company. I couldn't have done it without them!"

Kendall SummerHawk

Award-Winning Coach, IAWBC.org

Our Community

Testimonials from Industry Leaders

These messages come from business owners we’ve had the privilege to support—sharing their experiences, results, and what it’s like to have a payment partner focused on helping their business run smoothly and grow with confidence.

Each one offers a quick look at how the right payment setup, paired with real support, can remove friction, improve performance, and make it easier to keep revenue moving.

“Working with this team brought a fresh perspective to my content. Their ability to capture tone and emotion through words made a lasting impact on my readers. Each piece felt custom-built for my audience.”

Jenny

Blogger

Subscribe for Insider Growth Strategies

Receive actionable ideas to optimize your systems and increase conversions, information on industry events, partnership opportunities and more.

JOIN THE DIRECTPAY MAILING LIST

At DIRECTPAY, we believe how you get paid is just as important as what you sell. That’s why we go beyond basic payment processing to create seamless, secure, and strategic revenue systems. From merchant accounts to automation tools and expert support, our mission is to help your business run smoother, scale faster and get paid with confidence.

Pages

Information

Address

150 Motor Parkway Suite 401

Hauppauge, NY 11788

Call Us

800-326-9897

© DIRECTPAY Inc. All Rights Reserved

DIRECTPAY is a registered Independent Sales Organization of Wells Fargo Bank, N.A., Concord, CA.

DIRECTPAY is partnered with START Merchant Services, a registered MSP of Elavon Inc., a subsidiary of U.S. Bancorp.